Starting a business is exciting, but one of the first and most crucial decisions you’ll have to make is choosing the right type of business structure. The business structure you choose affects everything from daily operations and taxes to your personal liability and ability to raise capital. This guide will help you understand the various types of business structures, their advantages and disadvantages, and how to choose the best one for your needs.

What Is A Business Structure?

A business structure, simply put, is the legal framework under which your company operates. It determines how your business is organized, how it’s taxed, and the level of personal liability you’ll face as an owner. Choosing the right structure is crucial because it affects everything from your day-to-day operations to your long-term growth potential.

As a business owner, you’ll need to think about a few factors when choosing a structure:

- Liability protection: How much personal risk are you willing to take on?

- Tax implications: Different structures have different tax treatments.

- Flexibility: Some structures are easier to modify as your business grows.

- Complexity: Certain structures require more paperwork and compliance.

- Funding options: Your structure can affect your ability to raise capital.

Overview Of Common Types Of Business Structures

There are five primary business structures:

- Sole Proprietorship: A business owned and operated by one person.

- Partnership: A business owned by two or more people.

- Corporation: A legal entity separate from its owners.

- Limited Liability Company (LLC): A hybrid business structure combining elements of a corporation and a partnership.

- Cooperative: Often focused on providing goods or services to members at competitive prices.

Let’s look at each one in depth.

Sole Proprietorship

A sole proprietorship is the simplest business structure. It’s essentially a one-person operation where you, the owner, are the business. This is the most straightforward type of business structure, and it’s often the default choice for many entrepreneurs.

In a sole proprietorship:

- You are the business, and the business is you.

- There’s no legal separation between you and your business.

- You have complete control over all decisions.

Pros:

- Easy and inexpensive to set up

- Simple tax filing (business income is reported on your personal tax return)

- Complete control over business decisions

Cons:

- Unlimited personal liability for business debts and legal issues

- Limited ability to raise capital

- Can be challenging to build business credit

Think of your local freelance graphic designer or a neighborhood dog-walking service. These often start as sole proprietorships due to their simplicity and low startup costs.

When is a Sole Proprietorship Right for You?

A sole proprietorship is often the best choice for small businesses with low startup costs and limited risk. If you’re just starting out and testing the waters, this structure might be suitable. However, as your business grows and becomes more complex, you will have to consider other options.

Partnership

When two or more individuals decide to go into business together, a partnership is often the structure of choice. There are three main types of partnerships:

- General Partnership (GP)

All partners share equally in profits, management responsibilities, and liabilities. - Limited Partnership (LP)

Includes both general partners (who manage the business and assume liability) and limited partners (who are typically investors with limited liability). - Limited Liability Partnership (LLP)

Provides personal asset protection for all partners while allowing them to actively manage the business.

Pros:

- Shared financial burden and combined expertise

- Relatively easy to form and operate

- Pass-through taxation (profits are taxed on partners’ individual returns)

Cons:

- Potential for disagreements between partners

- Shared liability in general partnerships

- Complicated exit strategies if a partner wants to leave

Many law firms and accounting practices operate as LLPs, allowing partners to share in the management and profits while protecting their personal assets.

When is a Partnership Right for You?

Partnerships can be a good option for businesses where multiple people have complementary skills or when pooling resources is necessary. However, it’s important to have clear agreements in place regarding responsibilities, profit-sharing, and decision-making to avoid conflicts.

Corporation

A corporation is a legal entity separate from its owners (shareholders). This type of business structure creates a separate legal entity distinct from its owners (shareholders). There are two main types of corporations:

- C Corporation

- The standard corporation model

- Can have an unlimited number of shareholders

- Taxed separately from its owners

- S Corporation

- Limited to 100 shareholders

- Pass-through taxation (like a partnership)

- Must meet specific IRS requirements

Pros:

- Limited liability protection for shareholders

- Easier to raise capital through stock sales

- Potential tax advantages, especially for larger businesses

Cons:

- More complex and expensive to set up and maintain

- Double taxation for C Corps (corporate income and shareholder dividends are taxed separately)

- Extensive record-keeping and reporting requirements

Most publicly traded companies are C Corporations, while many smaller, privately held companies opt for S Corporation status for tax benefits.

When is a Corporation Right for You?

Corporations are often suitable for businesses with high growth potential, those seeking investor funding, or those with significant liability concerns. However, the complexity and ongoing costs might not be justified for smaller businesses.

Limited Liability Company (LLC)

An LLC is a hybrid structure that combines elements of corporations and partnerships. It’s become increasingly popular among small to medium-sized businesses because of its flexibility and liability protection.

Key features of an LLC:

- Separates personal assets from business liabilities

- Flexible management structure

- Pass-through taxation by default, with the option to be taxed as a corporation

Pros:

- Personal asset protection

- Flexibility in management and profit distribution

- Less paperwork than a corporation

Cons:

- More complex to set up than a sole proprietorship or partnership

- Self-employment taxes for members

- Varying state regulations

Many tech startups and real estate investment companies choose the LLC structure for its liability protection and operational flexibility.

Cooperative

While less common than other structures, cooperatives (co-ops) offer a unique model where the business is owned and operated by its members for their mutual benefit.

Key features of a cooperative:

- Owned and controlled by members who use its services

- Profits are distributed among members

- One member, one vote principle

Pros:

- Shared ownership and democratic control

- Potential tax advantages

- Can foster strong community ties

Cons:

- Decision-making can be slow due to the democratic process

- Limited access to capital

- Complex regulatory requirements in some jurisdictions

Many agricultural businesses, such as dairy farms or organic food producers, operate as cooperatives to share resources and market power.

Alternative Types Of Business Structures

While sole proprietorships, partnerships, and corporations are the most common business structures, there are additional options to consider. These alternative structures often cater to specific business needs or industry requirements. For instance, cooperatives are owned and operated by a group of individuals who share in the benefits and risks. Limited Liability Partnerships (LLPs) combine elements of partnerships and corporations, offering limited liability to partners. Non-profit organizations are created to fulfill a specific social or charitable mission rather than generating profit. These alternative structures offer unique advantages and considerations, and it’s important to research their specific requirements to determine if they align with your business goals.

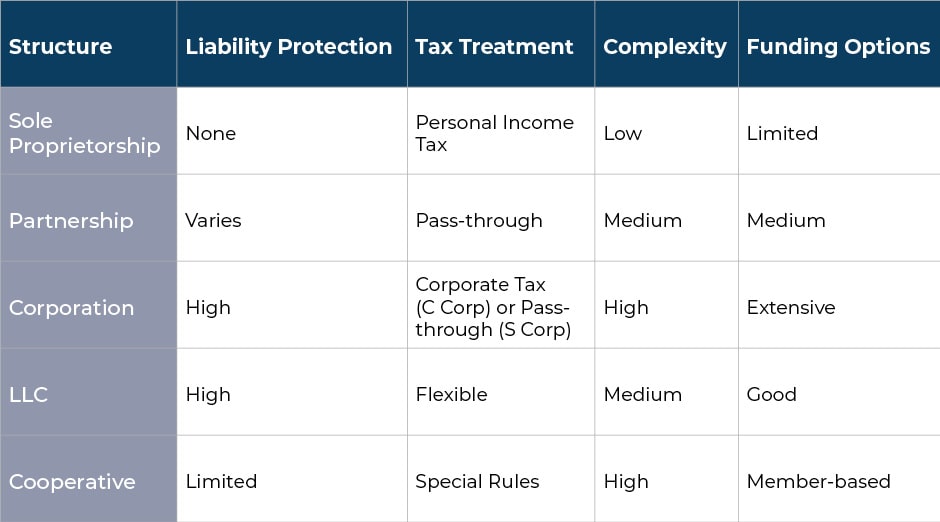

Comparing The Different Types Of Business Structures

To help you visualize the differences between these structures, let’s break them down in a comparison table:

When deciding on your business structure, consider:

- Your long-term business goals

- The level of liability protection you need

- Your preferred tax situation

- The complexity you’re willing to manage

- Your plans for growth and funding

Remember, there’s no one-size-fits-all solution. The best structure for your business depends on your unique circumstances and objectives.

Legal And Tax Considerations

When choosing a business structure, it’s necessary to understand the legal and tax implications, especially if you’re operating in both Canada and the USA.

Canadian Considerations

- Different provinces may have different requirements for business registration and reporting.

- The Canada Revenue Agency (CRA) has specific tax rules for each business structure.

- Some structures, like corporations, may offer tax advantages through income splitting.

U.S. Considerations

- Each state has its own rules for business formation and operation.

- The Internal Revenue Service (IRS) treats different structures uniquely for tax purposes.

- Some structures, like S Corporations, are specific to the U.S. tax system.

Cross-border Considerations

- Operating in both countries may require separate entities in each jurisdiction.

- Be aware of tax treaties and potential double taxation issues.

- Consult with experts familiar with both Canadian and U.S. business laws.

Given the complexity of these issues, it’s always wise to consult with tax professionals who specialize in cross-border business operations.

Factors To Consider When Choosing A Business Structure

Selecting the best business structure requires careful consideration of several factors. Here are some key things to think about:

- Liability Protection: Determine the level of personal risk you’re willing to accept. Some structures offer more protection than others.

- Cost of Setup and Maintenance: Factor in the fees associated with forming and maintaining different business structures.

- Control and Ownership: Consider how much control you want to keep over your business and how you plan to share ownership.

- Funding Options: Evaluate the ease of raising capital for each structure. Some options, like corporations, can attract investors more readily.

- Scalability: Think about your business’s growth potential and choose a structure that can accommodate expansion.

- Industry Regulations: Some industries have specific requirements for specific types of business structures.

By carefully weighing these factors and considering your business goals, you can make an informed decision about the best structure for your enterprise.

Decision-Making Process

To help you make an informed decision, create a checklist outlining the key factors that matter most to your business. Consider your liability concerns, tax implications, desired level of control, funding needs, and long-term growth plans.

While you can gather information from various sources, including online resources and business guides, it’s highly recommended to consult with financial professionals. They can provide tailored advice based on your specific circumstances and help you understand the complexities of business law and taxation.

With careful planning and consideration, you can establish a solid foundation for your business and set yourself up for long-term success. To help you manage and understand this process, MyBooks offers expert advice to guide you towards the best business structure for your needs. Contact us today for a free consultation.

FAQ

Sole proprietorship is typically the easiest and least expensive structure to set up.

Yes, you can change your business structure as your company grows or your needs change, but it may involve complex legal and tax implications.

Corporations and LLCs generally offer the strongest liability protection for owners.

Yes, you can hire employees, but you, the owner, remain solely responsible for all business obligations.

While possible, operating without a formal structure can expose you to personal liability and limit growth opportunities.

Yes, nonprofits can make a profit, but this profit must be used to further the organization’s mission rather than being distributed to owners or shareholders.