One of the biggest decisions for a business owner is deciding which accounting method to use. The main options in accounting are cash vs accrual, each one having pros and cons. Knowing the difference between cash and accrual accounting matters a lot for anyone, at any point in their company’s development.

In this article, we want to discuss the two accounting methods, the tax rules associated with each one and how you can figure out which one your business needs.

Understanding the Basics: Cash vs Accrual Accounting

At the core, the primary distinction between accrual accounting vs cash basis accounting lies in the timing of when revenue and expenses are recorded. Let’s explore the basics of both accounting methods.

- Cash Accounting: Under this method, revenue is recorded only when cash is actually received, and expenses are recorded only when they are paid. This method is typically simpler and better suited for smaller businesses or those with limited inventory.

- Accrual Accounting: In contrast, accrual accounting vs cash basis accounting records revenue when it is earned (regardless of when cash is received) and expenses when they are incurred (regardless of when payment is made). This method is more comprehensive and often preferred for larger businesses or those dealing with more complex financial transactions.

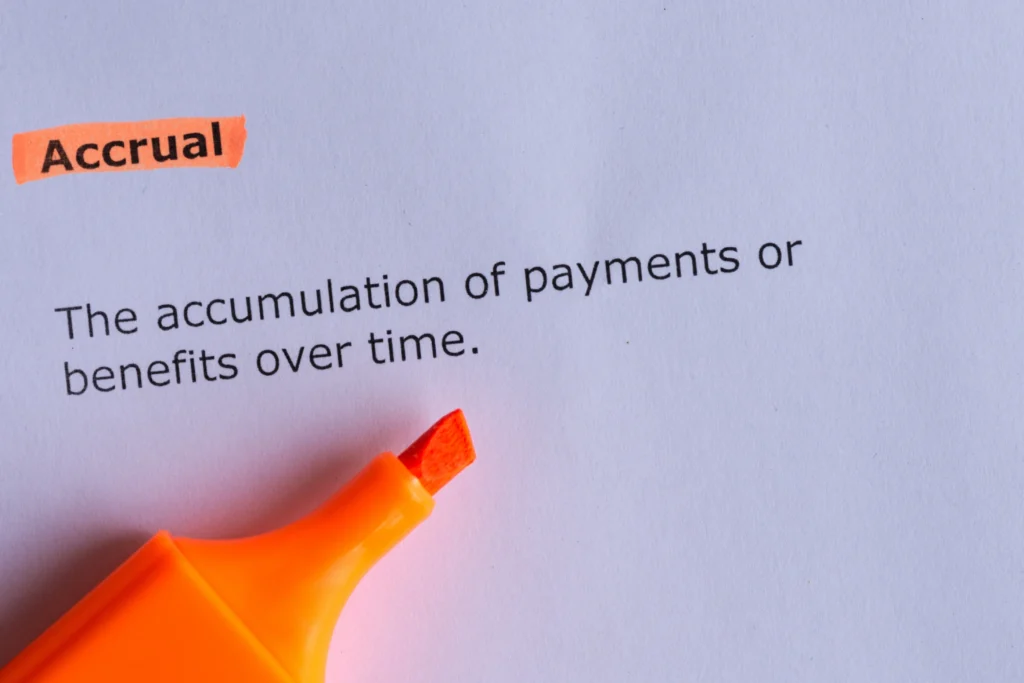

The Meaning of Accrual in Accounting

The meaning of accrual in accounting refers to the practice of recording financial transactions when they occur, rather than when cash is exchanged. This means that revenue is recognized when earned, and expenses are recorded when incurred, not when payment is made.

For example, if you deliver a product to a customer and invoice them, you will record the sale and revenue at that time, even if the customer hasn’t paid yet. Similarly, if you receive an invoice for office supplies but haven’t paid it yet, the expense is still recorded when the service or goods are received, not when the payment is made.

Cash vs Accrual Accounting: Key Differences

Understanding the difference between cash and accrual accounting is essential for choosing the right method for your Canadian business. Here’s how they compare:

Timing of Revenue and Expenses

The main distinction lies in when income and expenses are recorded:

- Cash Accounting: Records transactions only when money is received or paid. It reflects actual cash flow but may not show the full picture of financial obligations or income.

- Accrual Accounting: Records revenue when it is earned and expenses when they are incurred, regardless of payment timing. This provides a more accurate view of your financial position over time.

Complexity and Reporting

- Cash accounting is simpler to manage and may be suitable for very small businesses or self-employed individuals with minimal complexity (though CRA approval may still be required).

- Accrual accounting, required for most businesses under CRA rules, gives a clearer view of long-term financial health, particularly important for businesses with accounts receivable, payables, or inventory.

Tax Implications

In Canada, the Canada Revenue Agency (CRA) generally requires businesses to use the accrual method for tax purposes. Only certain types of businesses, such as farming or fishing operations, may use the cash method. Most sole proprietors, partnerships, and corporations must report income and expenses on an accrual basis, regardless of business size or revenue.

Financial Accuracy

Accrual accounting offers a more accurate and consistent representation of your financial performance by matching income with related expenses in the same period. This helps businesses make better financial decisions and meet reporting obligations with greater confidence.

Accrual vs Cash Method Tax Implications

When it comes to accrual vs cash method tax implications, there are several important considerations:

Tax Timing

- Cash Accounting: Taxes are paid on income when it is actually received. For example, if you send an invoice in December but receive payment in January, the income would be reported in January.

- Accrual Accounting: Income is reported in the period it is earned, not when payment is received. Using the same example, the income would be reported in December, even if the payment arrives in January.

Deductions and Write-offs

- Under the accrual method, you can deduct expenses when they are incurred, even if they haven’t been paid yet. For example, if you receive inventory and an invoice in December, you can deduct that expense in December—even if you pay in January.

- This method ensures that expenses match the revenue they help generate, providing better insight into your financial performance.

End-of-Year Tax Reporting

- Businesses using the cash method may have more flexibility in deferring income or accelerating expenses to manage taxable income.

- Accrual accounting requires precise matching of revenue and expenses to the periods in which they are earned or incurred, which leads to greater accuracy but less timing flexibility.

Accrual Accounting Benefits for Businesses

For growing businesses or those with complex financial transactions, accrual accounting offers several advantages:

- Better Financial Picture: Accrual accounting ensures that income and expenses are recorded when they occur, which gives a more realistic view of a business’s financial health. This method is especially useful for businesses that provide goods or services on credit or have significant inventory.

- Improved Decision Making: With accrual accounting, businesses can better assess profitability over a specific period, which aids in decision-making. For example, if you see that your business is generating significant revenue but also incurring high costs in the same period, you’ll be able to make more informed decisions about where to cut costs or improve efficiency.

- Required for Larger Businesses: Businesses with annual revenues exceeding $5 million are required to use accrual accounting. This requirement ensures that larger businesses are reporting their finances accurately, which is essential for external stakeholders like investors, banks, and regulators.

- Tax Deductions: Businesses using accrual accounting can deduct expenses as they are incurred, which allows for more efficient tax planning and better matching of income and expenses. This can provide significant tax advantages for larger or more complex businesses.

- Creditworthiness and Investment: For companies seeking investment or applying for loans, accrual accounting benefits for businesses include presenting a more robust financial picture to lenders and investors. Accrual accounting provides a clearer view of business performance, which can improve your chances of securing funding.

Looking for Help Choosing or Managing Your Accounting Method?

Whether you’re just starting out or looking to switch methods, having the right tools or experts can make the transition smoother. If you’re looking for a simple, cloud-based accounting solution or need professional help with your bookkeeping and tax filings, MyBooks Accounting offers both software and fully managed services tailored to small and growing businesses in Canada. Their platform supports both cash and accrual methods, and their team can help you stay compliant with CRA requirements.

Conclusion

Understanding the difference between cash and accrual accounting will help you make a more informed decision about your business’s accounting method, which will ultimately affect your financial strategy, tax obligations, and growth potential. Make sure to evaluate your specific needs and, if necessary, consult a financial advisor or accountant to determine the best approach for your business.

FAQs

Do investors prefer cash or accrual accounting?

Investors prefer accrual accounting because it provides a more accurate and complete picture of a company’s financial performance, including outstanding income and expenses.

Can I switch from cash to accrual accounting?

Yes, you can switch from cash to accrual accounting, but you must apply the new method consistently going forward and adjust prior-year records if necessary.

Do I need CRA approval to change my accounting method?

Yes, CRA approval is required if you want to change your accounting method, especially for income reporting. You must submit a request and provide reasons for the change.

Is cash or accrual accounting better for tax purposes in Canada?

Accrual accounting is generally required and preferred for tax purposes in Canada, as it aligns with CRA guidelines and provides more accurate income matching. Cash accounting is allowed only for specific businesses (e.g., farmers, fishers).

How does accrual accounting affect financial statements?

Accrual accounting improves financial statements by matching revenue and expenses to the period they occur, offering a clearer view of profitability and financial health.